Government-funded child investment accounts are becoming a point of interest for policymakers around the world.

Middle-income Mongolia serves as an interesting and lesser-known example: a country that has been implementing this program for two decades with impressive results, as reported by MiddleAsianNews.

Since 2005, Mongolia has had a cash transfer program for children (CTP), which guarantees monthly payments of ₮100,000 (about $30) for all children aged 0 to 17. These funds are deposited into special accounts in the children's names. The country's banks view this program as a reliable long-term source of capital and offer special children's savings accounts.

About one-third of households transfer the received payments to these accounts, allowing them to accumulate interest rates ranging from 11% to 13% per annum — which corresponds to the market rate for term deposits.

One of the key advantages of such accounts is the ability to automatically renew the deposit, which promotes the accumulation of compound interest over time — this feature is absent in other types of term deposits. Although early withdrawal of funds is possible, families opting for this lose almost all accumulated interest, creating an incentive for long-term savings.

Data from the Bank of Mongolia shows that since 2021, the balances in children's savings accounts have increased by 20% and reached ₮3 trillion ($840 million) in 2024, which is equivalent to more than 8% of the total volume of deposits in the banking sector. However, detailed data for analyzing savings at the individual child level is lacking, highlighting the need for further research in this area. A deep analysis of the dynamics of these accounts could reveal characteristics of their structure and transfer volumes that influence outcomes.

Research shows that having bank accounts positively affects financial behavior and well-being. These accounts contribute to reducing poverty levels and increasing opportunities: studies link them to increased savings, enhanced economic activity among women, and improved productivity in agriculture. Owning a personal account is also associated with better financial resilience and the ability to adapt to unexpected financial difficulties.

Moreover, receiving payments into official accounts helps develop financial skills through practical experience, while observing the increase in account balances strengthens trust in financial institutions and encourages long-term participation.

Mongolia's experience demonstrates that these mechanisms work at a significant level. According to Global Findex 2025 data, while only 75% of the adult population in low- and middle-income countries has access to financial institutions, in Mongolia, this figure reached nearly 98% since 2021. Although it is difficult to establish a direct link between the Child Financial Support Program and such outcomes, Mongolia's successes are commendable and warrant further study, noted the World Bank Group.

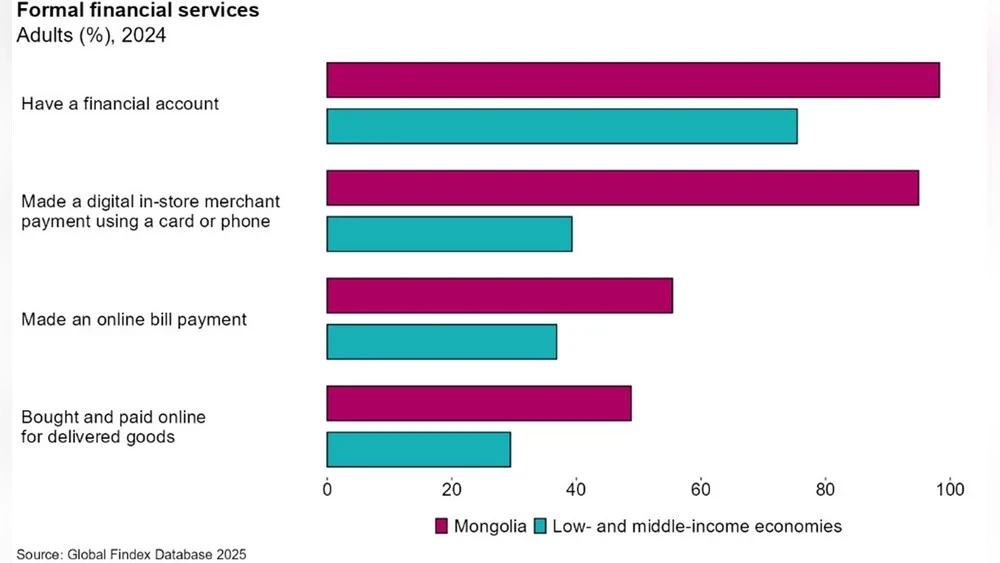

However, having an account is just the first step. Formal financial services are also widely used in Mongolia (see Fig. 1), made possible by the digitization of government payments, including salaries, pensions, and social benefits, which clients receive into their accounts.

As of 2024, 95% of Mongolia's adult population makes digital payments in stores using cards or smartphones, more than half shop and pay for goods online, and 70% pay utility bills directly from their accounts.

In low- and middle-income countries, only 39% of adults make digital payments in stores, about 25% shop and pay for goods online, and 37% pay bills over the internet. By global standards, the level of engagement in digital financial transactions in Mongolia is quite high.

Fig. 1: Mongolia shows a high level of adoption of digital financial services.

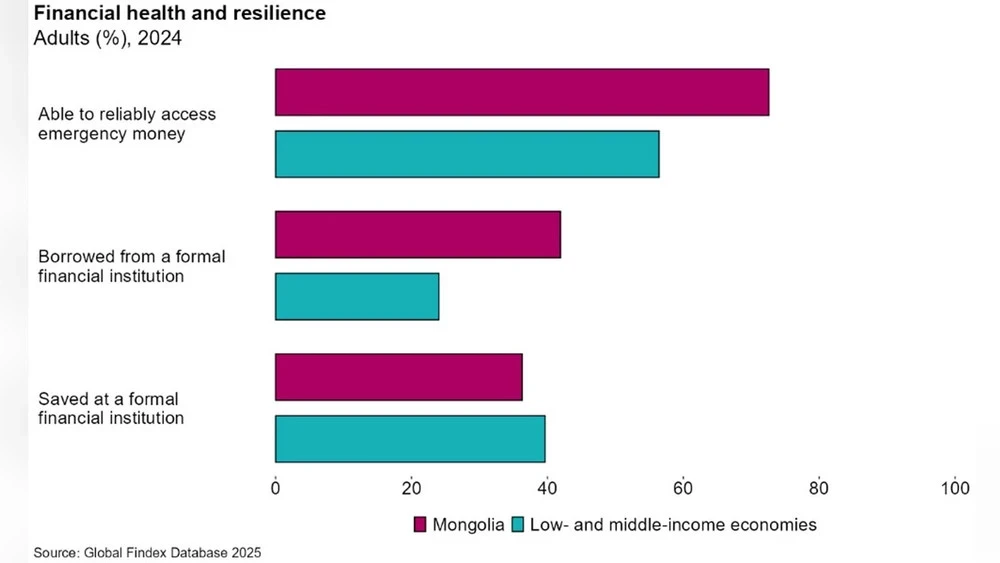

The high level of account ownership and active usage significantly impacts financial stability and resilience. Mongolia demonstrates impressive financial resilience indicators (see Fig. 2): about 75% of adults can quickly access emergency cash, which is one of the best results among developing countries.

This level of resilience may be linked to the widespread use of formal financial services, including a borrowing rate that is nearly double the average for low- and middle-income countries, and a level of formal savings similar to other economies.

Financial resilience is particularly important in Mongolia, where extreme weather conditions, such as dzud and harsh winter conditions, regularly threaten the livelihoods of the local population. One in four adults reports experiencing an extreme weather event in the past three years, and two-thirds of those have lost income or property. Interestingly, the level of financial resilience among people who have experienced disasters is comparable to those who have not faced such risks.

The developed digital financial ecosystem can serve as an important tool for vulnerable households to manage financial crises.

Fig. 2: The adult population of Mongolia demonstrates high resilience to financial shocks.

Mongolia is actively developing the child financial support program, which is one of many national initiatives aimed at improving access to financial services. It illustrates how early account opening combined with active usage can significantly enhance financial resilience. The experience of this country shows that such accounts can provide not only initial capital but also help develop financial skills, improve interactions with formal financial institutions, and lay the groundwork for long-term financial well-being.