The dynamics of changes in the financial habits of Kyrgyz citizens over the past four years is evident: while in 2020 the share of savings in the disposable income of citizens was 24.3%, by 2024 it sharply decreased to 10.8%. This indicates that the residents of the country prefer to meet their current needs, foregoing the creation of a financial "safety cushion."

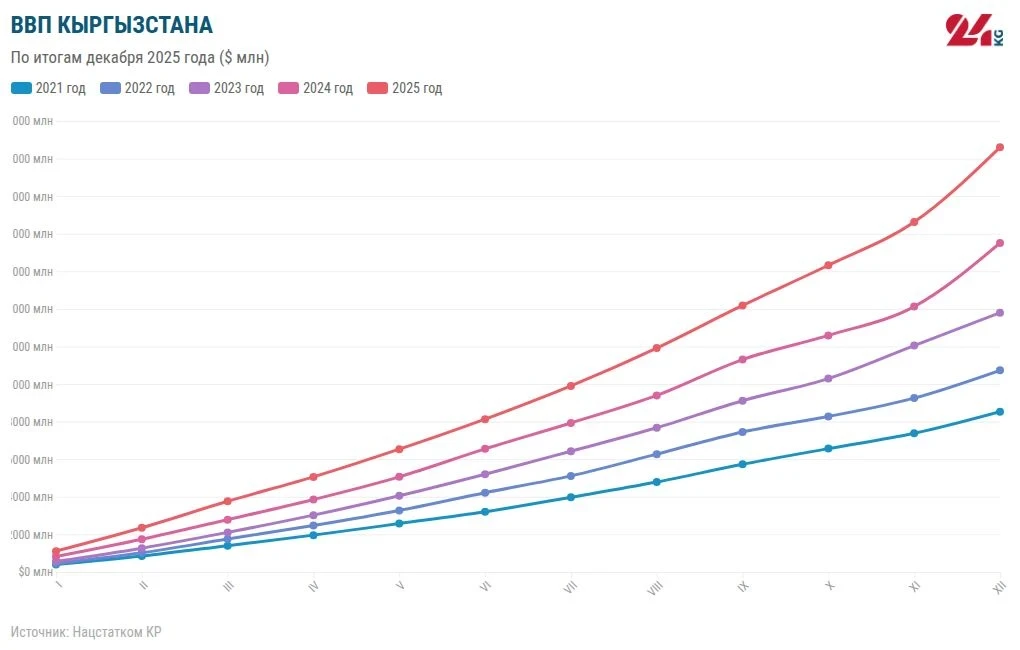

Statistical data confirms this trend: in 2024, the gross disposable income amounted to 1.8 trillion soms, of which almost 1.6 trillion was directed towards consumption. This is particularly noticeable in the household sector. If at the beginning of the decade, expenditures on goods and services accounted for about 75.4% of GDP, by 2024 this figure increased to 86.9%. It is important to note that over the past four years, negative savings values have been observed in Kyrgyzstan, indicating a troubling fact: the population spends more than it earns, covering the funding deficit through loans and microloans.

This scenario undermines the financial stability of society. When incomes are almost entirely spent on daily needs, people have no funds left for investments or creating reserves for emergencies. The country's economy becomes dependent on the level of consumption, and households become vulnerable to any external shocks, such as sharp price fluctuations, job loss, or a slowdown in economic activity.

Under current conditions, experts recommend revising financial strategies. The first step towards stabilization should be careful tracking of expenses: even simple accounting can help identify non-obvious financial "leaks." Having a minimal reserve capable of covering a few weeks of living expenses can prove critically important in emergencies. Furthermore, given the high share of consumption, loans can quickly become an excessive financial burden. Diversifying income through side jobs or freelancing, as well as developing personal skills, remain key ways to enhance financial resilience in the long term. The main goal today is not wealth accumulation, but minimizing financial risks through prudent expense management.

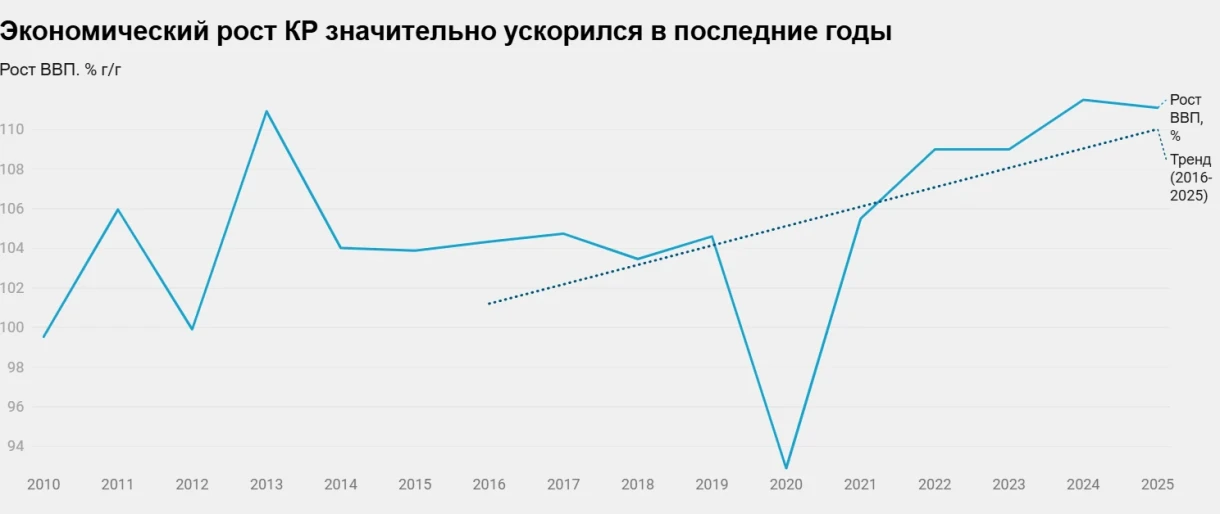

To better understand the historical context, it is worth paying attention to similar periods in the country's history. According to archival data from the National Statistical Committee, in 2010-2012, when the country was recovering from the crisis, the savings rate fluctuated between 12% and 15%. Later, in 2015-2017, against the backdrop of adapting to the conditions of the EAEU and an increase in remittances, the trend towards accumulation strengthened, reaching 18-20%. The peak level in 2020 (24.3%) was largely driven by the pandemic and the effect of deferred demand. The current decline to 10.8% is historically low for recent years, confirming that changes in the population's behavior have become irreversible.