Gas reserves in Europe are at a minimum, and LNG supplies are dwindling rapidly. We analyze whether the EU can avoid purchasing gas at exorbitant prices and how attractive gas futures are for investors, writes Alfabank.

Minimum Gas Reserves

As of March 22, the level of gas storage in Europe is just under 28.5% of total capacity, which is close to historical lows and significantly below average values for this time of year.

The situation in individual countries looks even more alarming: in the Netherlands, storage is at 6.6%, in Sweden — 14.6%, and in Croatia — 17.2%.

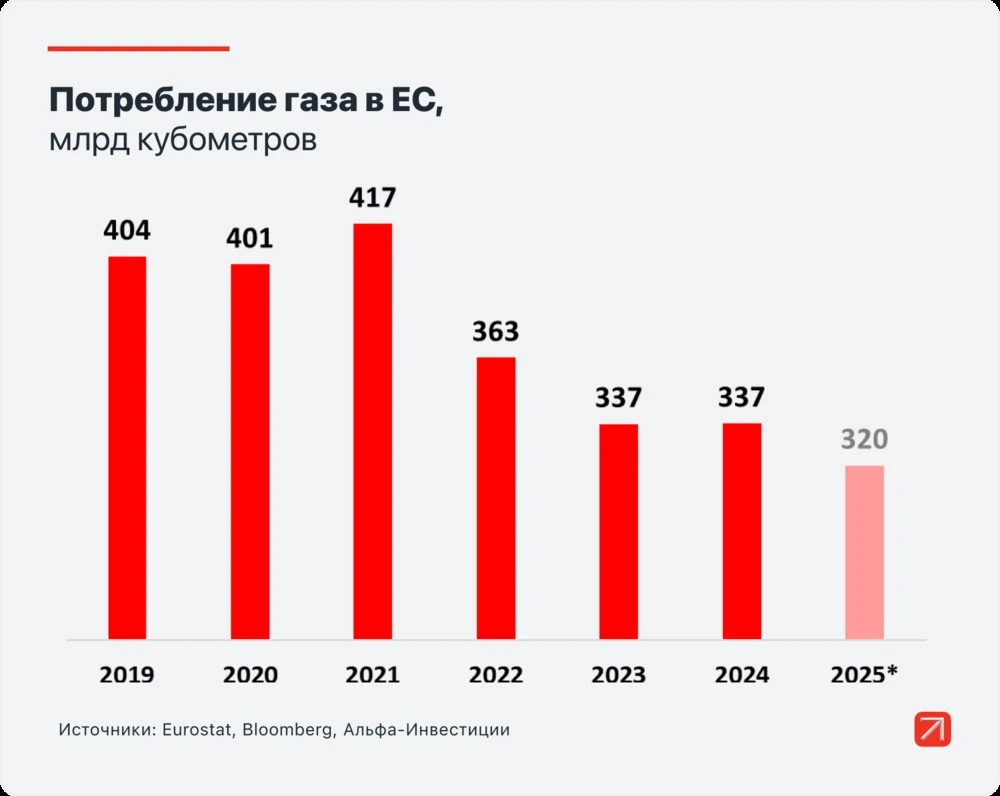

This indicates that by the start of the heating season in 2026-2027, Europe will need to purchase significantly more gas for storage than usual. To achieve 90% capacity by November, local traders will need to buy about 67 billion cubic meters of gas beyond normal consumption, which accounts for about 20% of total gas consumption in the EU in 2025.

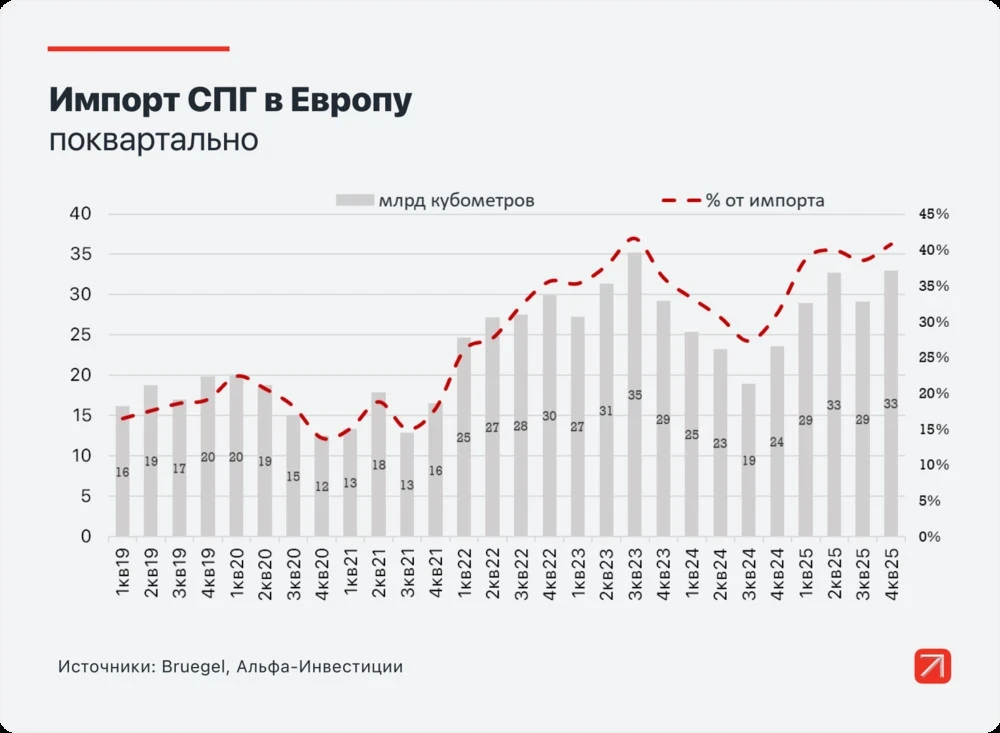

The challenge is that after the cessation of pipeline supplies from Russia, Europe primarily relies on LNG, and this share continues to grow.

Problems with LNG Supplies

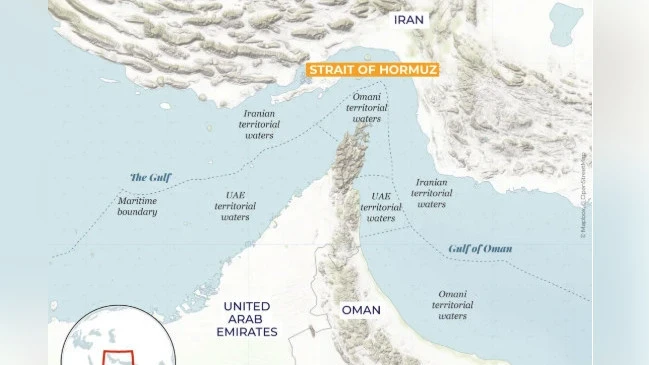

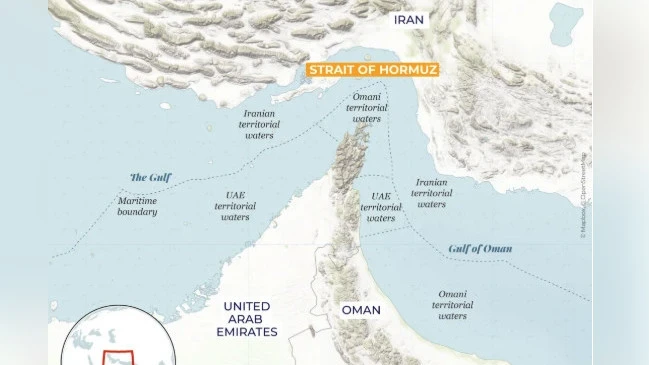

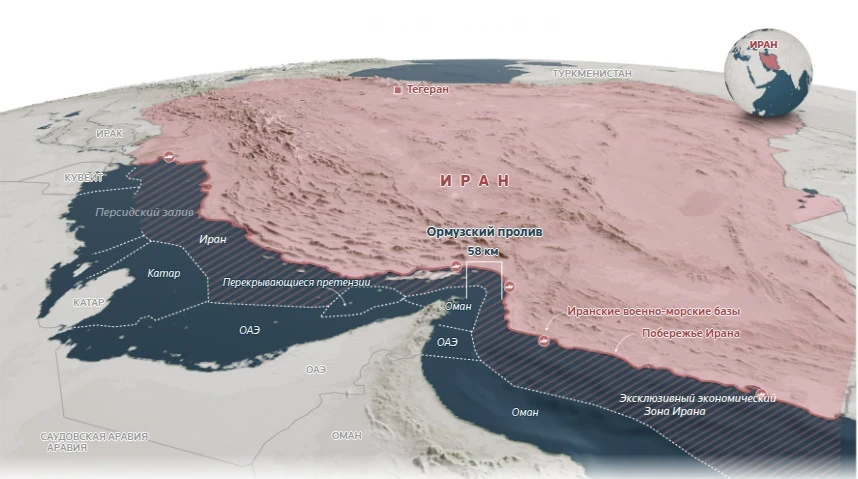

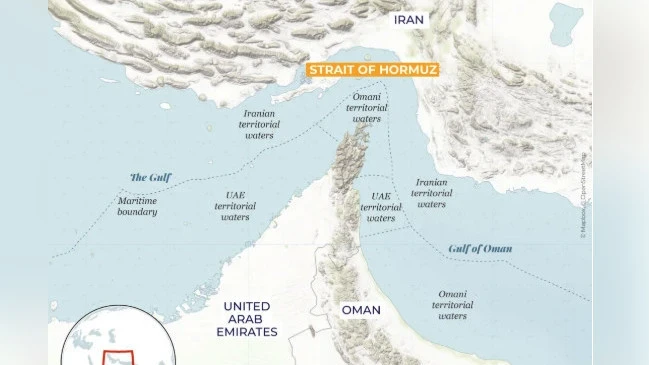

In March 2026, Iran blocked the Strait of Hormuz, halting LNG exports from Qatar, which account for about 20% of global supplies. Moreover, following an airstrike, about 17% of the country's production capacity was rendered inoperable for a period of 3 to 5 years, complicating the recovery of supplies even after the strait is reopened.

From the Middle East, the EU receives only 11.4 billion cubic meters of gas. However, the LNG market is interconnected, and the loss of a major supplier affects all consumers. Additionally, the EU plans to phase out Russian LNG, which supplied 20 billion cubic meters in 2025. This gas will not disappear from the global market, but its buyers will be found in Asia, making it unavailable for the EU.

Currently, the EU has virtually no alternatives to pipeline supplies: routes from Norway, Azerbaijan, and Algeria are already operating at full capacity. Meanwhile, about 18 billion cubic meters of gas from Russia still flows to the EU through Turkey, but given the current political situation, these volumes also remain uncertain. The EU aims to completely abandon these supplies by November 1, 2027.

Competition with Asian Countries

A significant portion of the LNG purchased by the European Union comes from the spot market, where free cargoes not demanded under long-term contracts are sold. Ships with such cargoes can quickly choose where to send them — to Europe or Asia, depending on the offered conditions.

During the summer, due to the heat in Asia, electricity consumption for air conditioning and refrigeration increases, leading to higher demand for natural gas. During peak consumption periods, Asian countries, especially China, begin to actively purchase additional gas on the spot market, creating competition for Europe. This, in turn, leads to rising LNG prices.

This summer, LNG supply from Qatar, which mainly sells gas under long-term contracts, will be lower than usual due to the aforementioned 17% of production capacity being out of service. With a prolonged closure of the Strait of Hormuz, the losses could be significantly greater.

At the same time, the EU will be forced to buy more gas to replenish reserves, leading to increased competition for free cargoes. In the event of abnormal heat, prices could rise significantly.

These risks are not yet fully reflected in prices.

What Awaits Europe

The demand for gas has increased due to a cold winter, while supplies have decreased. This creates two possible scenarios for the EU's gas balance:

• Reduction in consumption, which could lead to economic stagnation. This process has already begun since 2022, but it is progressing slowly — a sharp disconnection of consumers could have catastrophic consequences, including a negative impact on the political careers of those making such decisions.

• Offering a higher premium for LNG — which, in turn, will lead to further price increases. Since the beginning of March, TTF gas prices, the main index in the region, have more than doubled. However, this may not be the limit. Current quotes do not account for the risks of prolonged closure of the Strait of Hormuz and increased demand in Asia due to summer heat. If these risks materialize, TTF quotes could break the records of 2023.

Moreover, the consequences may also affect 2027. Especially if reserves cannot be fully restored by winter, and a cold winter returns. In that case, high prices may persist into the following year.

Investment Strategies: Gas Futures

The main strategy is to buy TTF gas futures with the expectation of further price increases or sharp price fluctuations. Profits can be made through TTF futures available on the Moscow Exchange. In the context of increased interest in this topic, trading activity and liquidity of futures have increased, facilitating comfortable opening and closing of positions, taking advantage of volatility.

To date, the highest number of transactions is taking place with the nearest TTF-3.26 contract. From April 1, the main trading will be conducted with the next TTF-4.26 futures. These futures are quoted in euros per MWh, and 1 lot corresponds to one MWh. Thus, purchasing gas futures can also serve as a hedge against the weakening of the ruble against the euro.

Those who have not yet traded natural gas futures on the Moscow Exchange are advised to familiarize themselves with special materials, such as how to trade natural gas: Henry Hub and TTF on the Moscow Exchange.

Investment Strategies: Stocks

High gas prices are currently beneficial for Russian producers who continue to supply gas to the EU. Higher prices mean greater revenue for companies like Gazprom and NOVATEK.

Both companies supply roughly the same volumes; however, NOVATEK's share of supplies to the EU is significantly higher, which may have a greater impact on the financial results of this company. Additionally, NOVATEK has the ability to redirect its tankers to Asia, making its exports more resilient under current conditions, despite sanctions.

Gazprom's share of supplies to the EU is small, but it could benefit from changes in the political situation if the EU decides to restore imports through some pipeline routes. In this case, the LNG shortage and high dependence on it could become strong arguments for cooperation with Gazprom. However, at the moment, political sentiments in the EU do not favor optimism.